At first glance, the emerging energy arrangement involving Shell, Venezuela, and Trinidad and Tobago appears to be a lifeline. After years of declining domestic gas production, underperforming LNG trains, and a struggling downstream sector, the prospect of accessing vast Venezuelan reserves seems almost providential. Billions of cubic feet of gas, just kilometres away, ready to be tied back into Trinidad’s infrastructure, processed, and exported, is the kind of opportunity that could extend the energy sector’s lifespan by decades.

But beneath the optimism lies a more uncomfortable question: whose deal is this really? While Trinidad and Tobago may host the infrastructure, process the gas, and facilitate exports, the underlying reality is that the country is stepping into a new and unfamiliar role, not as a producer, but increasingly as an importer of natural gas, and that shift changes everything.

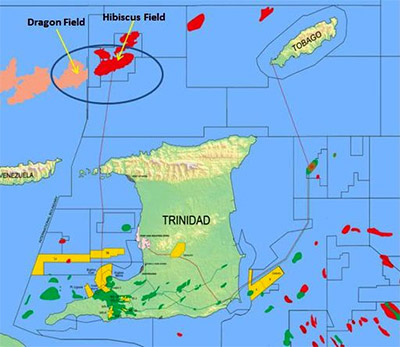

The numbers are compelling. The Dragon field alone holds an estimated 4.2 trillion cubic feet of gas, with the broader Mariscal Sucre and Loran-Manatee areas pushing total reserves to roughly 20 trillion cubic feet.

For a country grappling with declining output, this is transformative. It offers the possibility of reviving Atlantic LNG, restoring capacity to plants in Point Lisas, and stabilising an industry that has long been the backbone of the national economy, but access does not equal ownership.

The gas belongs to Venezuela. The royalties and taxes generated from production will flow primarily to Caracas, not Port of Spain. Trinidad and Tobago’s role will be to process, add value, and export. That is not insignificant, but it is also not the same as controlling the resource itself. This is where the risk of being short-changed begins to emerge.

Shell, which already holds a dominant position in Trinidad’s LNG sector, is effectively positioning itself as the central orchestrator of this arrangement. Its long-term strategy, spanning acquisitions, infrastructure control, and cross-border resource integration, has placed it in a position of considerable leverage.

As one energy expert noted, this is part of a “long game” that Shell has been playing for over a decade. In that game, Trinidad and Tobago is both a partner and a dependent.

On the one hand, the country provides critical infrastructure, such as LNG plants, pipelines, and processing facilities, which makes the monetisation of Venezuelan gas feasible. On the other hand, it now relies on external reserves to sustain its energy economy, creating a vulnerability.

If supply terms shift, if geopolitical tensions escalate, or if contractual arrangements disproportionately favour external stakeholders, Trinidad and Tobago could find itself locked into a system in which it bears operational responsibility without commanding strategic control.

There is also the geopolitical dimension. Venezuela remains a politically complex and sanctioned environment. Any arrangement involving its energy resources is inherently exposed to external pressures, particularly from the United States. A change in sanctions policy, diplomatic relations, or regional stability could disrupt supply flows overnight. This is not a theoretical risk; it is a structural one.

The global landscape is shifting

At the same time, the global energy landscape is shifting. Disruptions in major LNG-producing regions, including recent instability in the Middle East, are reshaping supply chains and creating new opportunities.

Trinidad and Tobago is well-positioned geographically and infrastructurally to benefit from these shifts, but opportunity without strategy is exploitation waiting to happen. Trinidad and Tobago will only get the best of this deal based on how it negotiates its position.

If the country approaches this as a passive recipient of gas, grateful for supply and eager for revival, it risks being marginalised in the value chain. Processing fees and downstream activity may provide short-term relief, but long-term wealth generation will remain limited.

However, if the Government recognises the leverage it still holds, the outcome could be very different. Trinidad and Tobago’s infrastructure is not easily replicable. Its LNG facilities, trained workforce, and established export routes are critical to efficiently monetising these reserves. That gives the country bargaining power if it chooses to use it. To mitigate the risks, several steps are essential.

First, contractual transparency must be non-negotiable. The public must understand the terms under which national assets are being utilised. Hidden agreements breed distrust and often mask unfavourable conditions.

Second, the Government must negotiate for greater value capture. This could include favourable processing fees, equity participation, or mechanisms that ensure a meaningful share of downstream profits remains within the country.

Third, diversification is critical. Relying too heavily on imported gas from a single source creates dependency. Trinidad and Tobago must continue to explore domestic reserves and alternative energy strategies to avoid becoming structurally reliant on external supplies.

Fourth, geopolitical risk management must be built into every agreement. Contingency plans, flexible supply arrangements, and diplomatic engagement are essential to navigate the uncertainties surrounding Venezuela.

Finally, there must be a broader national conversation about what this shift means. Becoming an importer of gas is not just an economic adjustment; it is a strategic transformation. It redefines the country’s role in the global energy system.

This deal has the potential to revive an industry, protect jobs, and stabilise the economy. But it also has the potential to entrench dependency, dilute national control, and shift value elsewhere.

The difference will not be determined by the size of the reserves or the scale of the investment. It will be determined by whether Trinidad and Tobago negotiates from a position of strength or settles from a position of need.

{kind=link}